Return Analysis

In this section we’re going to build on everything we’ve learned, both strategically and mathematically. We’ll take the “money in,” the number described by the story of our Growth Milestones, and the “money out,” the number explained by our Exit Strategy. Here, we will try to make the math work.

Let’s do this with a seed investment out of our hypothetical $75M VC Razor Fund II.

VC Razor Fund II, First Investment

Jeff and Mark were excited to announce they had closed Fund II, oversubscribed at $75M. The new fund had the same investment strategy as VC Razor I: 10-12 early stage deals, typically starting with seed investments. The difference this time is that they could average closer to $6M per startup rather than the $4-5M in Fund I.

They have found a startup they are very excited about. A couple of Carnegie-Mellon undergraduate engineering students have dropped out of school to create a co-working productivity tool. This is right in the sweet spot for VC Razor Ventures: young, smart, tech-savvy entrepreneurs who already have a product in the marketplace gaining traction, but who could really use the guidance of some investors who have been there before. Jeff and Mark already have some great ideas about how to gain market share quickly.

The young founders, we’ll call them YFs, have pitched that they need $100,000 to get to profitability. They say that, with their current user base and the additional customers a new marketing campaign would bring in, they would never need additional funding.

Jeff and Mark don’t exactly disagree, but they have a bigger vision. True, the YFs only need about $100,000 right now to do some marketing and add some product features. However, if that investment works, VC Razor Ventures would want to raise a $1M Series A round to start going to the next level with new product features that would appeal to a larger market.

Assuming the YFs hit the Series A milestones, Jeff and Mark think there is a potential to go after a bigger market segment with another round of financing with the goals of reaching 100,000 paying users, 3 specific new product features and at least one strategic partnership with a major tech company. Building a company that could handle that growth would require a Series B in the $5-10M range.

At that point, Jeff and Mark could see things going a few different ways. The strategic partner mentioned above could be interested in acquiring the startup, probably in the $75-100M range, or a C round could position it well for a $200-300M exit. Another possibility is that more strategic partners may come on board, bringing the idea of an IPO into consideration.

VC Razor Ventures coached the YFs about this possible bigger trajectory, including multiple rounds of VC financing, as opposed to the $100K to profitability strategy the YFs had pitched. VC Razor Ventures projected, assuming milestones were hit and the economy didn’t implode, that the startup could raise several rounds of funding. On the back of a napkin, they sketched out this potential scenario:

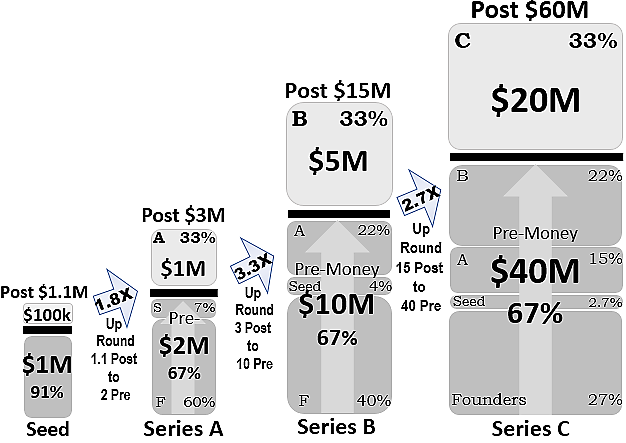

- Seed round: $100K investment on a $1M pre-money valuation

- Series A: $1M on $2M

- Series B: $5M on $10M

- Series C: $20M on $40M

- Exit: $200M

Adding all the rounds of investment above, the total raised would be approximately $26M. If they could find a buyer in the $200M-$300M range, it would be a terrific success for both the founders and VC Razor Ventures. They estimated that the founders might retain 20% of the equity for exit, worth around $40-60M at exit.

Breaking it Down

As we’ve said many times already, when VCs first look at a startup, we are thinking holistically about the entire life of the investment, not just the Series A. We will map out in our heads a best guess as to every round of investment on the way to exit.

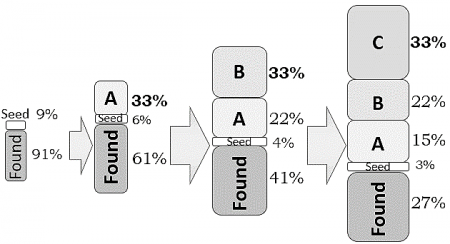

In Mark and Jeff’s scenario, we start with a $100,000 seed round, followed by a Series A, B and C. Each follow-on round dilutes the ownership of earlier shareholders. In this case, each follow-on round happens to be diluting by 33% (1 on 2, 5 on 10 and 20 on 40). This is just a coincidence that falls within the 20-40% norm.

We’ll walk through the math in a bit, but here is an overview of dilution from each round:

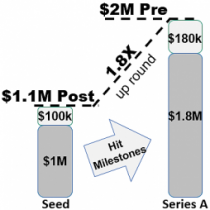

Every round projected is an up round, of course, as we are forecasting success. The seed investment of $100,000 on a $1M pre-money yields a post-money of $1.1M. The Series A has a pre-money of $2M. This implies that milestones must have been hit, as the value has increased approximately 1.8X.

Every round projected is an up round, of course, as we are forecasting success. The seed investment of $100,000 on a $1M pre-money yields a post-money of $1.1M. The Series A has a pre-money of $2M. This implies that milestones must have been hit, as the value has increased approximately 1.8X.

The seed investors’ $100,000 investment is now worth $180,000 (on paper), and the $1M worth of stock owned by the founders, as determined by the seed round pre-money valuation, is now worth $1.8M. The image to the left shows the pre-money breakdown; the $1M investment is not in there yet. (Series A is a 1 on 2 round.)

Similarly, between the A and B rounds, we are projecting an up round from the Series A post-money of $3M to the Series B pre-money of $10M, or a 3.3X increase. Finally, from Series B to Series C we see another increase of 2.7X, from a post of $15M to a pre of $40M.

{end of excerpt}